Limited Partners evaluating Venture Capital funds expect to see early returns, measured in terms of DPI (Distributions to Paid-In Capital). However, VC funds DPI can take years to materialize. Understanding the timeline of VC fund performance helps LPs make well-informed capital allocation decisions. Many top-performing funds may not show robust distributions in the first few years. This post explores the data behind VC Funds DPI generation and the factors that influence it—such as the J-curve effect, illiquidity, and capital recycling.

In This Article

Why VC Funds DPI and TVPI Matter

I start by defining metrics such as DPI and TVPI in Venture Capital, how they are used, and why they matter to LPs (Investors in VC funds) and GPs (General Partners—the Venture Capitalists deploying those funds).

You can skip this section if you already know all about these notions.

DPI (Distributions to Paid-In Capital) and TVPI (Total Value to Paid-In Capital) are the two metrics used to assess a VC fund’s performance.

DPI measures the actual cash distributions a VC fund has returned to its LPs, representing realized or “real” performance. LPs use DPI to understand how much capital they’ve gotten back relative to their investment (or “paid-in capital”).

A DPI of 1x means the fund has returned 100% of the initial capital. For example, a $100 million fund with a DPI of 0.3x returned only 30 million dollars, which is bottom quartile performance in VC. A total DPI over 3x is solid top-quartile territory.

Read the article below for more details on VC funds' performance over 30 years.

Go Further: Venture Capital Returns: True Lies?

In contrast, TVPI includes the unrealized value (or residual value) of investments still held by the fund. It gives LPs a broader picture of the fund’s total performance by including both distributions and the estimated current value of the remaining investments.

TVPI = (Residual Value + Distributions) / Paid-In Capital

Unlike DPI, TVPI can fluctuate as market valuations change. TVPI can be problematic for LPs because it is subject to manipulation or over-optimistic valuations.

One big issue is that TVPI is often based on last-round valuation.

In bubble markets, these paper gains inflate proportionately with the startups’ values. Social Capital’s Chamath Palihapitiya has been vocal about how inflated valuations in Venture Capital can create a “Silicon Valley Ponzi scheme”, creating an illusion of success that attracts more capital from new Investors, even though the underlying companies may not be as valuable as they appear.

This is one of my favorite VC videos of all time.

Pro tip: Subscribe to my YouTube playlist of VC-related videos here!

Research by Will Gornall and Ilya Strebulaev on unicorn (startups valued at over $1 billion) valuations further supports this skepticism. They found that unicorns are often overvalued, primarily due to the way their valuations are structured through private funding rounds. The artificially inflated TVPI gives LPs a distorted view of a fund’s actual worth, overestimating performance.

Watch this webinar for detailed explanations, with concrete examples, on these issues (members: click here).

The Data on VC Funds DPI Performance

While reliable sources of data on VC funds performance are rare due to the private nature of the asset class, efforts have been made in recent years to provide industry professionals with more analyses.

What follows is based on recent data shared by Carta, a fintech platform offering services for startups and VC firms.

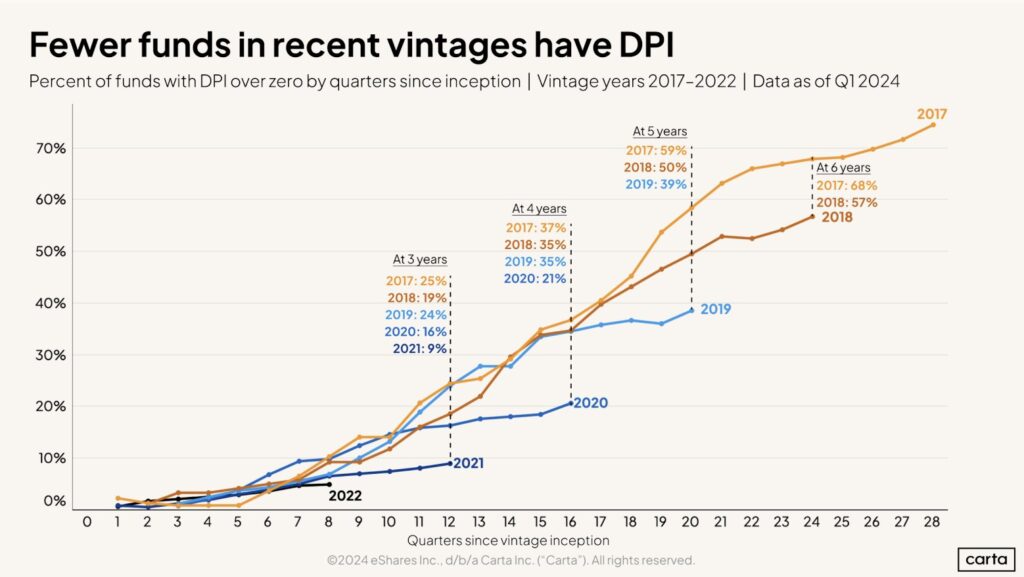

The Carta Q1 2024 VC Fund Performance report offers performance trends across 1,803 venture funds spanning vintage years 2017 to 2022. The data is sourced from Carta’s client base, focusing exclusively on U.S.-based funds operating as direct Venture Capital Investors (not funds of funds).

This slide sparked many conversations on the web, which I’ll cover later.

The graph illustrates the VC funds DPI trends for vintages from 2017 to 2022, highlighting how recent funds lag behind older ones in achieving meaningful DPI.

For example, at the 3-year mark, only 9% of 2021 vintage funds have achieved DPI greater than zero, compared to 25% for 2017 vintage funds—a 16-point gap.

The trend remains true at the 4-year mark (21% for the 2020 vintage vs. 37% for the 2017 ones—again, a 16-point gap) and at the 5-year mark (39% for the 2019 vintage vs. 59% for 2017–a whopping 20-point gap).

As LPs, we don’t think there is cause for any alarms.

Beezer Clarkson - Sapphire Partners

Many observers claimed the trend highlighted by Carta’s data shows that more recent funds are taking significantly longer to return any capital to their LPs, indicating a delay in liquidity compared to earlier vintages.

However, it may also be due to 2017 being an exceptional vintage. It beats even the 2018 vintage by 10 points! One explanation could be that funds launched in 2017 benefited from the exceptional 2020-2021 VC bubble and many firms profited to exit with high returns.

Industry professionals offered two alternative explanations for the data.

Performance Gap for Recent Vintages: The substantial gap between the DPI performance of 2017 funds and newer vintages highlights how challenging the exit environment has become for recent funds, compounded by market corrections and lower liquidity.

DPI as a Lagging Indicator: The data underscores that DPI takes time to develop, with newer vintages struggling to distribute capital early on. Funds generally require several years to mature and realize their investments before achieving meaningful DPI.

Additionally, a potential sample bias in the Carta report could influence the observed DPI trends, as the analysis primarily focuses on smaller and emerging funds. With 60% of the funds in the dataset being under $25 million and only 10% over $100 million, the performance dynamics might be different compared to larger, more established funds—making it harder to generalize the findings.

I’ll address the second point in the following section, with benchmarks from leading market players.

How Long Does It Take For VC Funds DPI To Show Traction?

To understand how long it takes for VC funds to demonstrate significant DPI performance, I analyzed data shared by prominent industry experts.

Their data provides a nuanced view of the timeframes required for funds to start delivering returns to LPs, challenging some common assumptions.

Data From Sapphire Partners

Beezer Clarkson is a partner at Sapphire Partners, a well-known LP firm that invests in early-stage VC funds. Her perspective matters because Sapphire Partners specializes in backing emerging managers, making their data a valuable resource for understanding the DPI trajectory of newer funds.

We leveraged our database of funds that have returned capital, and on average funds get to 1x DPI by year 8.

Beezer Clarkson - Sapphire Partners (Source: X)

In her analysis of the Carta report, Clarkson noted that, historically, it took VC funds in Sapphire’s portfolio approximately 8 years to reach 1x DPI—meaning they return the full amount of the invested capital to their LPs.

She emphasized the importance of capital recycling (see below), sharing data on two of her high-performing funds funds. While they showed a low DPI of 0.39x and 0.27x at year 5, they eventually reached impressive multiples of 11x and 8x.

Clarkson concludes that interim marks in year 5 do not provide indications of success or failure in VC funds. She added that several of her 3x funds had zero DPI by year 5.

Bonus: Read how Beezer Clarkson selects top emerging VC fund managers in the article below.

Data From VenCap

David Clark, a prominent VC analyst at VenCap, provided additional clarity on the factors that influence DPI timelines. VenCap has invested in venture funds globally since the 1980s, making their analysis and data highly credible.

In his study of 71 funds from the 2005-2008 vintages, Clark found that the correlation between year 5 DPI and the final performance was only 0.22. This indicates that early DPI does not reliably predict a fund’s eventual success.

Somewhat counter-intuitively, Clark’s research also showed that TVPI at year 5 had a higher correlation of 0.4 with final fund outcomes, suggesting that a combined view of both realized and unrealized gains offers a more accurate picture of potential performance.

The best-performing fund in the sample has a DPI of 12.3x. In year 5 its DPI was zero. Conversely, the best-performing fund after 5 years had a DPI of 1.28x. It's now at 2.55x.

David Clark - Vencap (Source: X)

Clark’s data primarily concerns funds that are $200 million and larger, with a focus on the sample of Series A and B funds.

These insights from Clarkson and Clark underscore the complexity of assessing VC fund performance through early DPI metrics. The consistent theme is that patience is essential for LPs, as the journey to meaningful distributions is long and often non-linear.

So why do VC funds take so long to perform well? There are a few key factors at play.

How The J-Curve Effect Impacts VC Funds DPI

The J-curve is a well-known phenomenon in venture investing. Early on, funds typically show negative or low returns as capital is deployed into startups that are still growing. It’s only over time—once these companies mature, scale, and potentially exit—that returns begin to pick up.