Understanding the Power Law: Do Venture Capitalists Take Enough Risks?

Once seen as mavericks making crazy bets shoulder-to-shoulder with the entrepreneurs they backed, Venture Capitalists are increasingly railed for focusing more on the "Capital" part of the job (managing money) than the "Venture" aspect (taking risks). Why do VCs today seem to have less appetite for risky bets? Do cautious Investors perform better? How do elite VC firms leverage the power law to generate top-quartile returns consistently?

In this post, I dive into the relationship between VCs and risk, first exploring why contemporary VCs appear more conservative compared to their trailblazing predecessors and how this change affects the industry’s dynamics. I also examine the approaches of top-performing VC firms, unveiling how they leverage the power law to achieve exceptional results. My analysis highlights that elite VCs have a different mindset when making investment decisions, which I call "promotion-focused," allowing them to take more risk to reach best-in-class returns.

In This Article

- Do VCs Take Enough Risk?

- The VC Power Law: Core Principles and Data

- How Elite VC Firms Generate Top-Quartile Returns

- Conclusion: tl;dr

Accelerate Your Learning: Watch Our Webinar!

Don’t just read about it, immerse yourself in the content through our companion webinar for this post! Engage with a multimedia presentation, discover all the referenced sources, and have your questions answered live! Click the “Watch Now” button to access the webinar. (Members: click here).

Do VCs Take Enough Risk?

While the question may seem inappropriate to outsiders, it has become relevant given the sharp increase in the number of Investors over the last two decades.

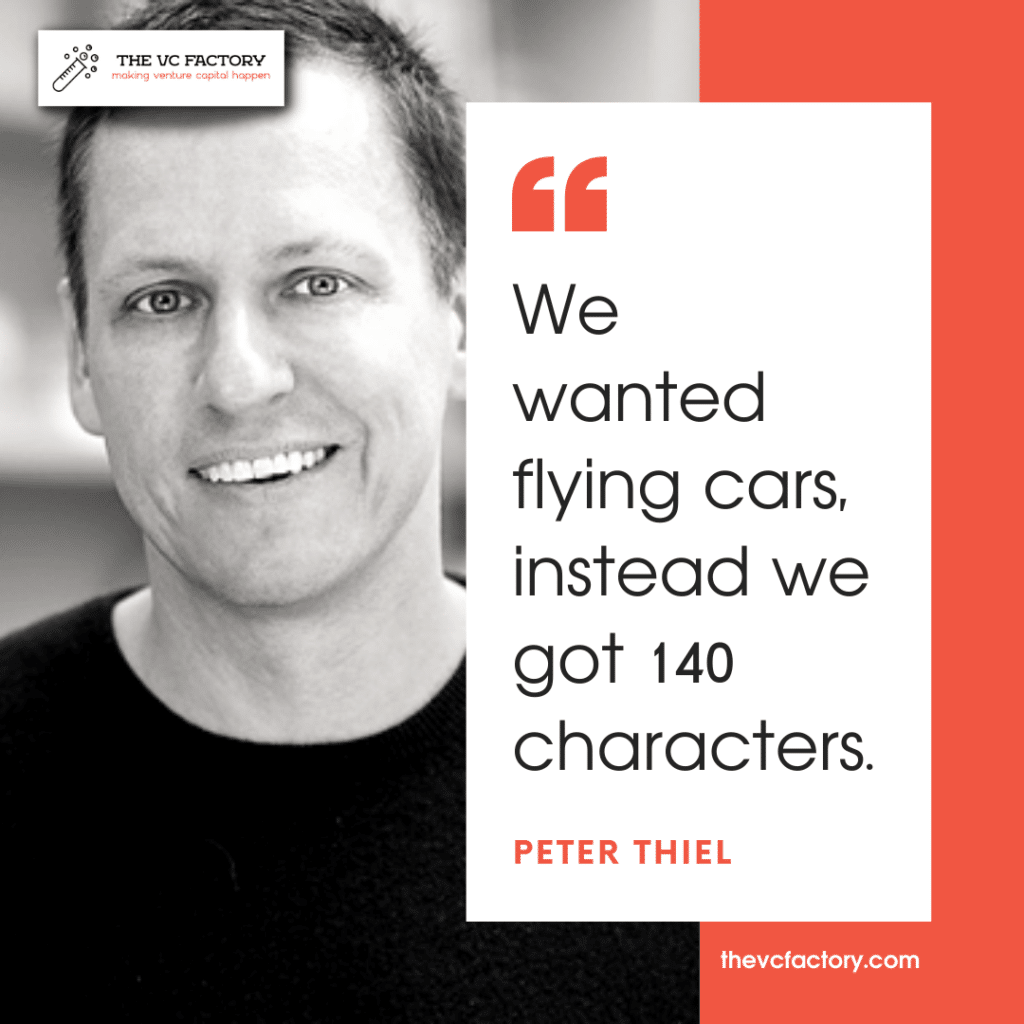

The Perception: 140 Characters, Not Flying Cars

As fundraising Founders will attest, phrases such as "We need to see more revenue before we can commit," "Come back later, it's a bit too early for us," and "Who else is looking at this?" are staples of Venture Capitalists' feedback. Many entrepreneurs complain that VCs do not take enough risks.

Peter Thiel, the PayPal co-Founder who's become a top voice in VC thanks to early investments in Facebook and Palantir, perfectly captured this prevailing sentiment. His famous phrase—instead of flying cars, we got Twitter—illustrates the gap between the lofty expectations of groundbreaking, world-changing innovations and the reality of incremental advancements funded by Venture Capital.

Thiel's words echo a broader critique of the VC community, suggesting that the boldness required to invest in visionary technology—the proverbial flying cars—has been supplanted by a preference for safer, more predictable ventures.

Is Deal Flow To Blame?

Some VC observers explain the current perception of risk aversion in VC not as a consequence of VCs becoming inherently more cautious, but as a response to the burgeoning startup ecosystem. As the number of startups has skyrocketed, identifying the next big success has become increasingly complex. The sheer volume of deals flowing through the pipeline requires a more nuanced approach to triage, sifting through many to find the few that hold potential.

There are about 4,000 startups a year that are founded in the technology industry which would like to raise venture capital and we can invest in about 20.

Marc Andreesen - a16z (source: website)

The abundance of investment opportunities may inadvertently push VCs towards a more conservative stance. According to these experts, the preference for safer bets does not stem from a diminished appetite for risk but an overwhelmed capacity to process and manage vast deal flow.

The industry has reached a saturation point where finding the diamonds in the rough is more challenging than ever, necessitating a refined, perhaps more cautious, selection strategy.

Screening deal flow quickly and effectively has indeed become a critical skill in the VC role, and I wrote several articles about it, such as the one referenced above. However, VCs must balance the necessity of rigorous deal evaluation with the innate drive to discover and invest in groundbreaking innovation.

My analysis points to a more profound shift in the nature of VCs, as the asset class matured in the last three decades.

A Profound Shift in Venture Capital

Venture capital has undergone a fundamental transformation over the years. Historically, VCs were closely involved with the companies they invested in, playing the role of hands-on company builders—admirably captured in the 2011 documentary Something Ventured. Today, the scenario has shifted significantly as many VCs have assumed the role of money managers, focusing more on financial returns than on nurturing innovative business ideas.

In the webinar, I highlight three consequences of this profound shift initiated by a rush of new entrants: lack of commercial talent, groupthink, and loss aversion.

Talent scarcity within the industry means fewer professionals can identify and nurture potential. New entrants to the field often struggle to gain a foothold, lacking the experience or networks of established players. An analysis by Social Capital's Chamath Palihapitiya revealed that a large proportion of the best VCs in history are exceptionally commercially driven individuals. Very few come from the product owner or engineering background many recent professionals in the industry possess.

Exceptional VCs like Fred Wilson, Michael Moritz, Bill Gurley, Jim Goetz, Alfred Lin, Peter Fenton, and a handful of others are unbelievably commercial.

Chamath palihapitiya - Social Capital (Source: All-In Podcast)

Groupthink can take root within recently created VC firms, leading to homogeneity in decision-making and an aversion to bucking the trend. It is characterized by the group members' tendency to minimize conflict and reach a consensus without critically testing, analyzing, and evaluating ideas. Individual creativity, uniqueness, and independent thinking are often overridden by the collective pressure to conform to the perceived group consensus. Groupthink is linked to herd mentality, which is the inclination for individuals’ thoughts and behaviors to align with those of a group they belong to. I analyzed the effects of VC groupthink in the article below.

Loss aversion is another key factor influencing Venture Capital today. The instinct to safeguard existing capital (or one's reputation) can eclipse the willingness to pursue innovative and risky opportunities that could lead to significant advancements or disruptions in various sectors. This conservative mindset can inadvertently prioritize preserving the status quo over catalyzing change. Loss aversion extends beyond the initial investment decision, negatively affecting reinvestment decisions in portfolio companies struggling to grow.

The problem with the "playing it safe" mentality that has gradually come to dominate VC is that historically, the majority of VC returns have been made by a small number of investments. High-risk, high-reward bets have the potential to yield exceptional outcomes, yet the inclination to avoid losses can deter VCs from making such bold moves. Recognizing and understanding this power law is crucial for VCs to embrace the potential for outsized returns, necessitating a departure from prevalent risk-averse attitudes.

The VC Power Law: Core Principles and Data

The power law is a fundamental feature of Venture Capital, as data analysis shows that VC funds' returns tend to follow such a skewed distribution. Before we dive into elite VCs' use of this law, I explain where it comes from and provide ample evidence using real-world data.

What Is The VC Power Law?

In statistics, a power law is a type of heavy-tailed probability distribution characterized by the principle that a small number of occurrences have a disproportionately large impact. This means that in a dataset described by a power law, the most significant items occur rarely, but their impact is exceptionally high compared to the rest.

Power laws are seen in various natural phenomena and human activities, where they describe relationships between two quantities such that a relative change in one quantity results in a proportional relative change in the other quantity, regardless of the initial size of those quantities.

The biggest secret in VC is that the best investment in a successful fund equals or outperformss the entire rest of the fund combined.

Peter Thiel - Founders Fund (Source: ZEro To one)

In the context of Venture Capital, the power law implies that most returns in a VC's portfolio come from a tiny fraction of investments. These breakout hits can return the value of the entire fund or more. For an early-stage investor, a 3x return on the whole portfolio requires a handful of investments to yield returns many multiples higher than the initial stake. These outliers, often called "home runs," are the essence of a successful VC capital deployment strategy.

Why do these outliers matter so much? Because startup successes are not incremental but often exponential. A startup that hits the right market with the right product at the right time can grow rapidly, resulting in outsized returns for the early investors who took the risk to back them. This is contrasted with a more conservative investment approach, where the aim is to make smaller, more frequent wins.

The power law also helps explain why Venture Capitalists can endure many failed investments. The rare successes more than compensate for the failures, generating enough returns to make the entire portfolio successful. This tolerance for failure is integral to VC, but it requires a mindset attuned to the power law—seeking out those rare opportunities with the potential for hyper-growth and industry disruption. I call this mindset a "promotion focus" and detail it below.

Example: The Famous Fred Wilson Post

Many Investors, including myself, were introduced to the power law by a 2009 post from Union Square Ventures' Fred Wilson, one of the highest-performing VCs of this generation. Although we now have more data than he did then, the demonstration remains correct.

Wilson begins by addressing a fundamental question: What constitutes a good return in Venture Capital? Using the acquisition of Pure Digital by Cisco for $590 million. Venture Capitalists invested $95 million in the company, which, assuming they owned half of its equity, represents a return of just over 3x their money. While seemingly impressive, Wilson notes that this return might be considered moderate, especially for high-profile firms like Benchmark and Sequoia.

Using an analogy from baseball (I'll provide more color on that later), Wilson explains that early-stage Investors like Union Square Ventures operate under the "1/3, 1/3, 1/3" principle:

- Lose their entire investment in one-third of the cases

- Break even or make a small return in another third

- Generate substantial returns in the remaining third

To achieve a 3x return on the entire portfolio, early-stage Investors need to aim for an average of 7.5x return on the successful third of their investments. This target is critical for delivering positive outcomes to Limited Partners (LPs), as I demonstrate with ample data in the article below.

Go Further: Venture Capital Returns: True Lies?

Wilson further illustrates that for Union Square Ventures' 2004 fund, one investment would have to generate $125 million to return the entire fund. Given USV's $10 million average ticket, it would represent a 12.5x return.

Fred Wilson's breakdown exemplifies how understanding the power law is essential in Venture Capital, revealing that success isn't about minimizing failures but maximizing successes. This mindset shift is vital for Investors, as it underscores the importance of identifying and supporting those rare, high-potential startups that can deliver outsized returns.

Power Law: The Data

In the webinar, I review multiple analyses and datasets pointing to a power law in VC distributions. While the categories between fail, average returns, and outliers are not as equally divided as Fred Wilson suggests, it is clear that a small number of investments generate most of a fund's returns.

Click here to watch an extract of the webinar (Members: access all our webinars here).