Should Investment Decisions Rely on Intuition or Data?

Early-stage Investors seem to rely on little else than their gut to make multi-million dollar bets on fledgling startups—and their Founders. How do the best VCs mix their intuition and other sources of information to make informed decisions? What can we learn from the latest research on our brain and judgment-making heuristics in VC? In this post and companion webinar, I analyze the weight of intuition and data in the process used to make Venture Capital investment decisions. I also give practical examples of how Venture Capitalists should train their intuition to incorporate data and avoid mistakes.

In This Post

Accelerate Your Learning: Watch Our Webinar!

Don’t just read about it, immerse yourself in the content through our companion webinar for this post! Engage with a multimedia presentation, discover all the referenced sources, and have your questions answered live! Click the “Watch Now” button to access the webinar. (Members: click here).

The Role of Intuition in VC Investment Decisions

It is undeniable that intuition plays a role in Venture Capital investing, as uncertainty prevails in entrepreneurship.

Entrepreneurship Is About Gut-Driven Decisions

Entrepreneurs often rely on their intuition to make decisions due to the high-stakes, fast-paced nature of starting and growing a business—where waiting for complete data can mean missing crucial opportunities.

This reliance on gut feelings is grounded in cognitive science, suggesting that intuition is a form of rapid, unconscious processing that amalgamates past experiences, knowledge, and cues from the environment to guide decision-making in uncertain situations.

Successful entrepreneurs are known for making intuition-based decisions, often "betting the house" with little more than a strong gut feeling. For instance, when Steve Jobs returned to Apple in 1997, he made the intuitive decision to simplify the product line drastically, a move not immediately obvious from the data but pivotal in Apple's turnaround.

Intuition is a very powerful thing—more powerful than intellect, in my opinion.

Steve Jobs - Apple (Source: Harvard Business Review)

Steve Jobs often emphasized that intuition guided many of his decisions at Apple. He trusted his gut feeling to create products that he and his friends would want, leading to innovations that often preceded market demand. This approach underpinned Apple's strategy, focusing on product simplicity and user experience, which became hallmarks of the company's success.

VC Investment Decisions Rely On Little Data

Venture Capital investing involves navigating through uncertainty and, in some way, attempting to predict the future, making decisions often based on intuition rather than solid data.

The problem with data is that it makes it challenging to imagine the exponential growth curves in nascent industries. Bill Gates' 1995 memo about the internet is a prime example. While only 0.4% of the world's population was using it at the time, he called it a "tidal wave" and didn't care about being mocked publicly on TV to push for its wider adoption.

Jack Ma had no business plan, zero revenue, and maybe 35-40 employees. But his eyes were very strong. He had strong, shiny eyes.

Masayoshi Son - Softbank (Source: Bloomberg)

Sofbank's Masayoshi Son's investment in Alibaba is a prime example of intuition driving monumental investment decisions. Masa, captivated by Jack Ma's vision and determination after just one meeting, decided to invest in Alibaba based on the conviction he saw in Ma's eyes, rather than on detailed financial analyses. This intuitive decision led to one of the most lucrative investments in Venture Capital history, showcasing the immense potential of trusting one's instincts in identifying future successes in the tech sector.

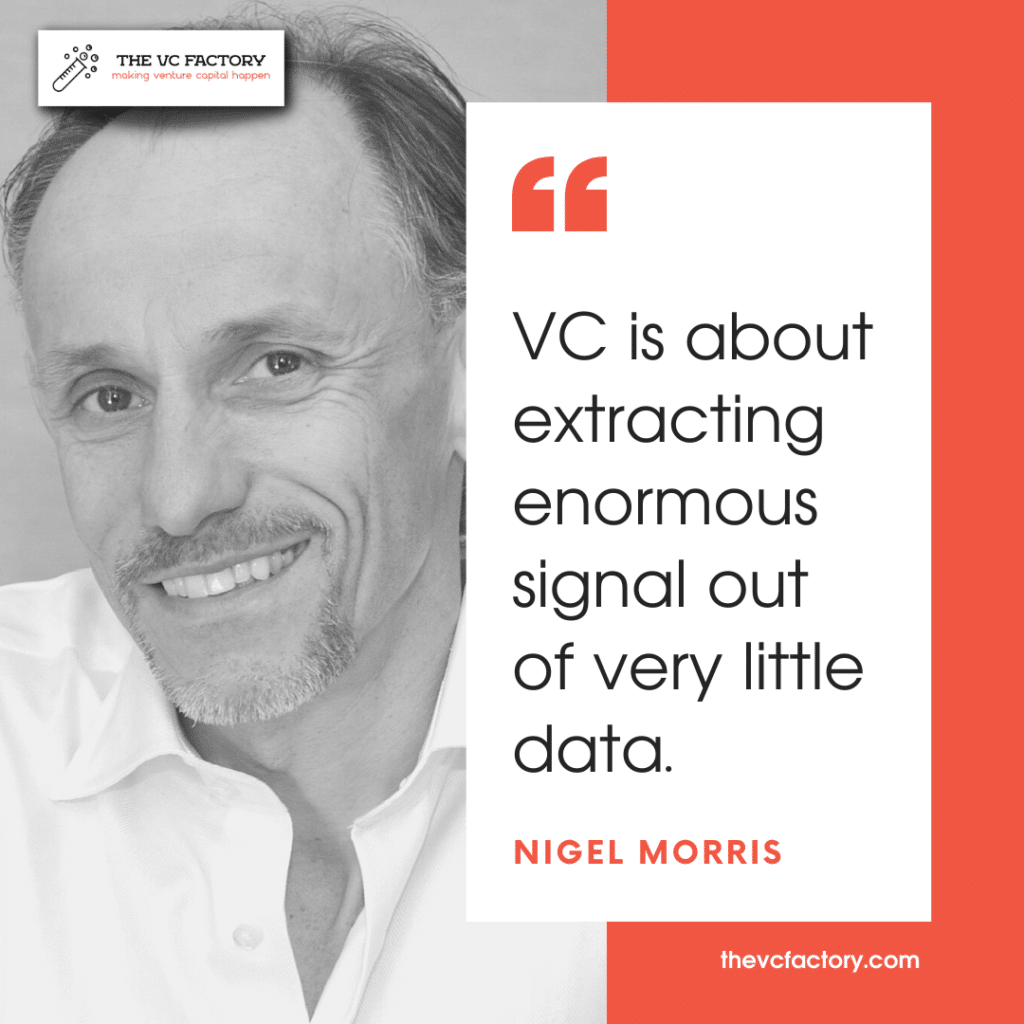

Since data is scarce in early-stage VC investing, Investors must develop a capacity to interpret signals, which primarily relies on intuition. Nigel Morris, the former Capital One co-Founder who now leads QED Investors, a fintech-focused VC firm, explained that the uncertainty in VC made it more challenging to make decisions than helming a $20-billion market cap company.

The Problem With Relying On Intuition To Make Investment Decisions

For all the glamour and hype, intuition-based investing is more often incorrect than successful.

The "Nostradamus Effect" of Tech Predictions

The narrative of successful Founders and Investors making prescient decisions thanks to superior intuition suffers from survivorship bias, as someone making poor gut-based decisions will not be remembered.

A "Nostradamus effect" skews our perception, making us remember the few predictions that turn out to be true while forgetting the multitude that do not materialize. This selective memory can often give an inflated sense of predictability in fields where uncertainty is the only certainty.

Famously wrong predictions about technology illustrate this point. IBM's Thomas Watson widely underestimating computer demand, 20th Century Fox's Darryl Zanuck's skepticism towards the impact of television, or Robert Metcalfe's doubts about the internet's scalability serve as stark reminders. These instances, rooted in intuition and the context of their times, underscore the challenges and risks of forecasting in technology.

The black-swan events of the past forty years—the PC, the router, the Internet, the iPhone—nobody had theses around those. So what’s useful to us is having Dumbo ears.”

Doug Leone - Sequoia (Source: New Yorker)

One striking commonality is how vested those who made these predictions were in them being true. IBM sold punch-card tabulating systems when Watson made his famously wrong prediction about computers, Zanuck saw television as a competition of going to the movies, and Metcalfe sold extranets.

As Sequoia's Doug Leone suggests, technological disruptions are unpredictable. Investors need to have their ears on the ground to decipher the weak signals announcing their success.

I dive into these two points—cognitive biases leading to wrong predictions and the need to collect more data—in the companion webinar to this article.

Intuition Breeds Cognitive Biases Lethal To Sound Investment Decisions

The problem with intuition is that it gives rise to cognitive biases. The work of psychologists Amos Tversky and Daniel Kahneman is seminal in this area. They introduced the idea that making investment decisions based on intuition may lead to error in the wrong circumstances.

Biases present in VC investing include confirmation bias, which occurs when Investors seek out information that reaffirms their preconceived notions, disregarding evidence to the contrary. Priming can influence decisions when recent exposure to a certain idea or theme unconsciously influences responses to related topics. Groupthink can lead to poor decisions and outcomes as the desire for harmony or conformity results in a dysfunctional decision-making process where dissenting viewpoints are suppressed. Narrow mental models limit the Investor's thinking and can cause them to overlook potential investment opportunities that do not fit within their established frame of reference. I detailed these biases in the article below.

VC biases lead to two kinds of mistakes in investment decisions.

Errors of commission happen when a decision is made to move forward with an investment despite warning signs to the contrary. Masa Son's investment in WeWork is a notable example. Despite various concerns about the company's business model and sustainability, SoftBank continued to provide significant bridge funding after the IPO failed, throwing good money after bad. The eventual turmoil and near-collapse of WeWork exposed the potential consequences of such biased investment decisions.

Errors of omission occur when Venture Capitalists miss out on a significant opportunity. A classic case is Benchmark's decision not to invest in Google's Series A round. The firm failed to see the potential that Google's novel algorithm could have on the world of search and advertising, a misstep that can be attributed to the biases affecting their decision-making process. This error of omission resulted in missing out on what would become one of the most influential companies of the digital era.

In the webinar, I analyze how prominent Investors stayed away from AirBnB due to mental limitations and how they could have avoided this mistake by collecting more data.

In the next section, I'll discuss the significance of using data to make investment decisions. I argue that VC is a data-driven asset class, insofar as data analysis is woven into every step of the process.

Data Is At The Heart Of Venture Capital Investment Decisions

From deal flow management to due diligence, investment committees, and Board monitoring, collecting and interpreting data is part and parcel of the VC investing process.

Step 1. Deal Flow Management

Deal flow management is a crucial process in Venture Capital. Investors assess numerous potential investment opportunities to identify those with the highest potential. A study by Gompers et al. (2020) highlights the sheer volume of this endeavor, showing that the median US early-stage VC firm evaluated 119 deals annually for every single investment made—demonstrating the selective nature of the VC investment process.

The deal flow funnel involves several stages, each requiring more data:

- Considered per Close: Initially, a large number of potential deals are considered. In the 2020 study interrogating 195 early-stage VC firms, this number averages around 119 potential investment opportunities for each deal that is closed.

- Met Management: The Venture Capitalists then meet with the management teams of these companies, narrowing down the funnel significantly to about 34 meetings (29% of all opportunities considered).

- Reviewed with Partners: The remaining opportunities are then reviewed with the VC firm's partners, with approximately 11 reaching this stage (9% of all opportunities considered).

- Exercised Due Diligence: A deeper evaluation, called due diligence, follows, with around 4.6 opportunities undergoing this scrutiny (4% of all opportunities considered).

- Offered Term Sheet: Finally, a term sheet is offered to an even smaller subset, averaging 1.5 for every successful close (1.3% of all opportunities considered).

Each step filters the prospects more stringently, ensuring only the most promising ventures secure funding.

Step 2. Due Diligence

Once the investment opportunity reaches the next step in the process (pre-validation), due diligence starts. VC due diligence comprises a blend of exploratory and confirmatory steps to ensure a comprehensive understanding of the potential investment. The objective is to collect data to validate continuous interest in the opportunity and eventually present it to the Investment Committee.

The exploratory phase involves initial meetings and basic analysis to understand the company's business model, revenue plans, and market position. It is conducted by the deal team within the VC firm and is an iterative process: if partners express further interest, the deal team collects more data from the Founders.

Following this, the confirmatory part of due diligence dives deeper. It involves a robust investigation into the company's financial health, legal standing, and operational structure, often conducted by external experts (primarily financial auditors and legal counsels, depending on the startup's development stage). The article below goes deeper into the limits of VC due diligence.

Go Further: Why Venture Capital Due Diligence Fails

A crucial step of VC due diligence most Founders underestimate is the subtle cues and signals gathered by Investors during this discovery phase.

While VCs may initially claim they will make a swift go/no-go decision to Founders, the reality often involves a drawn-out process. This period allows VCs to gather crucial data by observing the entrepreneur's behavior over time. Important elements like how promptly entrepreneurs return calls or follow through on promises can be as telling as formal due diligence checks on legal documents or patent applications.

What Garage Ventures' Bill Reichert calls a "slow bake" approach, as opposed to a "microwave" deal, is favored by Investors as it offers deeper insights into the quality and reliability of the entrepreneurial team.